I grew up stretching every dollar like pizza dough, and that habit lives in my body. Some nights my chest tightens and the mind races, even when things are okay. I know that money anxiety can feel baked-in, and I’ve been there—mama, I see you.

In this guide I’ll name what’s simmering: the stress that shows up in your body, your daily life, and your health. It is not a moral failing. It is your nervous system trying to keep you safe.

We’ll build tiny routines—short prep steps for bills, a starter for savings, and quick scripts for late-night fear. You’ll get practical tips to use in real time: breathing breaks, snack-sized plans, and low-stress systems that fit into pockets of time with kids underfoot.

This kitchen is judgment-free. We keep what works, toss what burns, and season with grace. Ready to swap panic for a plan? Pour a cup of tea and let’s start where you are.

Key Takeaways

- Recognize how past scarcity maps to present stress and the body.

- Use tiny, repeatable routines to regain control of your finances.

- Quick calming practices ease the mind and protect your health.

- Keep frugal strengths and replace harsh rules with kinder habits.

- Reach for low-cost support and community when tasks feel big.

What money anxiety looks like in the United States right now

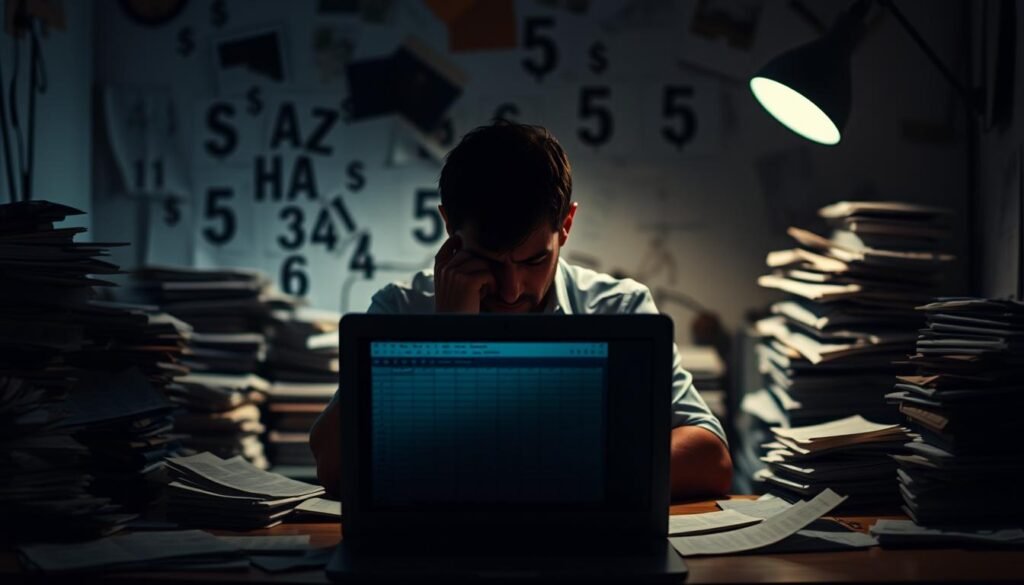

Inflation and a tight housing market have made routine financial checks feel urgent. For many households, a ping from the bank or a stack of unopened bills can trigger a rush of physical reactions.

Key signs and symptoms

Avoidance: You put envelopes aside and delay opening statements.

Analysis paralysis: Small purchases take forever to decide on.

Rumination and sleeplessness: Your brain loops worst-case scenes at night.

Present-day pressures

The APA found 87% of people named inflation as significant stress in 2022. That kind of uncertainty pushes normal worry into chronic financial anxiety.

Housing and daily triggers

- Rent and mortgages now eat larger shares of paychecks, so statements spike stress fast.

- Checking a bank account or a bill can cause stomach upset, headaches, or racing heart — real physical symptoms tied to stress.

- These reactions are common; millions of people face similar shifts in their financial situation.

Recognizing these patterns is the first step. When we name triggers, we can use small tools to calm the body before we touch the numbers.

Money anxiety

When childhood scarcity lives in your bones, small money decisions can feel like survival tests.

Growing up poor often teaches clever thrift. It can also wire fear and shame into how you handle cash.

That wiring shows up as hyper-control: tracking every penny, panicking when a bill shifts, and replaying worst-case stories in your mind.

Why early scarcity shapes reactions

Deprivation trains the nervous system to expect danger. Low or unstable income keeps the mind scanning for threats.

Rising expenses and inflation feel like the oven temperature changing mid-bake. You do the work, yet costs climb.

How common drivers feed financial fear

- Unsteady income makes cash flow unpredictable and raises baseline stress.

- Rising costs shrink purchasing power and trigger constant adjustments.

- Debt compounds quickly; high interest can create real despair and harm mental health.

- Shame blocks asking for help, which keeps worries private and heavy.

| Driver | Typical sign | Why it matters | Quick step |

|---|---|---|---|

| Low/Unsteady income | Constant alertness, tight cash buffers | Raises daily stress and reduces options | Track pay weeks and plan a small cushion |

| Rising expenses | Frequent re-budgeting, surprise shortfalls | Erodes savings and sense of safety | Freeze one spending category for 2 weeks |

| Debt | Dread, avoidance, higher interest costs | Can harm health and hope | List balances and tackle the highest rate |

| Uncertainty | Worst-case thinking, decision paralysis | Blocks forward movement | Set one tiny, repeatable routine today |

“I kept the thrift and let go of the panic, one small habit at a time.”

Step-by-step: practical techniques to reduce financial stress and regain control

Let’s walk through small, practical steps you can use today to calm your gut and take back control.

Pause and regulate

First, calm the cook: 60–90 seconds of breathing exercises or a two-minute meditation helps the mind settle. A quick walk works, too.

When your chest tightens, try belly breaths: in for 4, hold 1, out for 6. Repeat three times.

Get the numbers down

Create a simple recipe-style budget: list income, must-haves, and can-waits. Track one account for five minutes and stop.

Set tiny financial goals—$10 to savings or one small debt payment weekly—to build momentum.

Build safety and tackle debt

Open a separate emergency account and automate a small transfer on pay day.

List debts by interest rate; pay the highest while keeping minimums on the rest. NFCC counselors can help compare options.

| Technique | Why it helps | Quick step | Resource |

|---|---|---|---|

| Breathing/meditation | Calms the mind before decisions | 2-minute practice | Self-guided |

| Starter budget | Reduces financial stress by clarifying choices | One-page recipe card | Free apps or notebook |

| Emergency fund | Builds a safety buffer | Automate $5–$10/week | Bank account setup |

| Debt priority | Speeds payoff and lowers interest paid | List by rate, attack top balance | NFCC, CFPB tools |

Practical supports

Ask about unions or job supports, learn one marketable skill this month, and lean on friends or mutual aid for childcare or grocery swaps.

“I pause, do a quick breath, then check my Friday budget date.”

If things feel overwhelming, reach out: NFCC for budgeting and debt, CFPB tools to read the fine print, FTA for therapists who blend finances and emotion, or text CONNECT to 741741 for immediate support.

When financial anxiety affects health, relationships, and daily life

Financial strain sneaks into sleep, moods, and the way we show up at home. It can chop your rest into pieces. Poor sleep then makes decisions harder the next day.

Sleep, depression, and anxiety: why money worries keep you up at night

Nighttime worry about bills and debt rewires sleep. Over time, insufficient rest links to heart disease, high blood pressure, diabetes, worsened depression, and poorer mental health.

Simple night routines help. Try brief breathing or a short meditation before bed to settle the mind (two minutes can change the pace).

Risk behaviors to watch: gambling, hoarding, and substance use

Stress can push people toward quick fixes like gambling or using alcohol to numb fear. Studies show financial stress predicts greater gambling and later alcohol problems.

Hoarding—keeping multiples of items or expired food “just in case”—also rises under strain. These patterns are understandable and treatable with steady support.

How to talk about money at home without escalating conflict

Make short, kind money chats: set a time limit, one simple agenda, and one shared goal. Keep voices low and pause if things heat up.

Use validation: “I get that this feels scary.” Offer practical help, like researching options or joining a first call with a counselor.

| Issue | Sign to watch | Quick response |

|---|---|---|

| Poor sleep | Waking worried about bills | Set a 2-minute breathing practice before bed |

| Risk behavior | Gambling, hoarding, drinking to cope | Replace with safer substitutes; seek support |

| Household conflict | Late crisis talks, raised voices | Schedule a short, calm money chat with rules |

“When we validated each other first, the plan came easier.”

Conclusion

One last note: change happens in tiny, repeated steps—not giant leaps. That truth helps when money anxiety or financial stress tightens your chest.

You’re not “bad with money”—you learned survival skills during hard seasons. Be kind to that part of you and use a simple recipe: calm first, numbers second, tiny goals always.

Try a five-minute weekly budget date, automate a small savings transfer, and knock off one bite-sized to-do each time. Track wins—one bill paid, one calm talk, one better night of sleep.

Expect wobbles. We practice, we learn, and we get stronger. If emotions spike, lean on support: NFCC, CFPB tools, FTA therapists, or text CONNECT to 741741 for immediate help.

Your future isn’t decided by yesterday’s ingredients. With steady steps and clear goals, your finances and health will shift. I’m cheering you on—apron on, coffee in hand—one kind move at a time. 💛